Table Of Contents

SEC Regulation Best Interest (Reg BI) became effective on June 30, 2020, a little more than a year after the SEC formally adopted it. Reg BI established a “best interest” standard of conduct for broker-dealers when making recommendations to retail customers involving securities transactions. As part of Reg BI compliance, all advisory firms are required to submit a new form, which has been dubbed “ADV Part 3,” but is better known as Form CRS.

Reg BI Form CRS intends to clarify the relationship between firms selling securities products and their clients in terms of the services offered, fee structures, potential conflicts of interest, and the differences in the standard of conduct that govern BDs and RIAs. While the intent of the form is to reduce retail investor confusion, it has created confusion among the firms trying to meet its requirements.

What is the Form CRS?

The CRS disclosure requirements apply to SEC-registered advisors, including broker-dealers and RIAs, who have more than $100 million in assets under management. For advisors with less than $100 million in AUM who register with their states, there are currently only two states – Oklahoma and Rhode Island – that require Form CRS in addition to other disclosure requirements. Thus far, most state regulators have opposed the use of the form due to concerns about the disclosure document.

For investment advisors applying for SEC registration for the first time, the SEC has stated it will not accept any applications that don’t include Form CRS.

Where Form CRS Fits in the “Best Interests” Obligations of Financial Professionals

The “best interest” standard under Reg BI comes into play whenever a broker-dealer representative makes a recommendation to a retail customer involving a securities transaction or investment strategy that involves securities. This includes the opening of a new account. It is up to the broker-dealer to determine which types of interactions between its representatives and retail clients require adherence to the standard, requiring disclosure documents to a customer in connection with a recommendation.

The “best interest” standard is actually a set of obligations broker-dealers must fulfill to demonstrate they are not placing their own interests ahead of a retail clients’ interests. So, to meet the “best interest” standard, they must fulfill these four obligations:

Disclosure Obligation: Provide in writing all material facts describing the scope and terms of the client relationship, including disclosures of fees and costs, as well as material facts relating to any conflicts of interest related to the recommendation.

Care Obligation: That reasonable diligence, care, and skill were applied in making the recommendation using a “reasonable basis,” “customer-specific,” and quantitative criteria. This also means presenting “reasonably available alternatives” when considering the costs associated with a recommendation.

Conflict of Interest Obligation: Establish and enforce policies and procedures to address conflicts of interests related to recommendations by either disclosing of eliminating them.

The SEC Form CRS Rule

The Form CRS rule, which was adopted with the same Reg BI rulemaking package in June 2019, requires BDs and RIAs to submit an additional disclosure form on top of Form ADV Parts I and II. Unlike ADV Parts I and II, which can be somewhat voluminous, Form CRS is to provide, in two pages or less, disclosures of services, costs, potential conflicts of interest, and disciplinary histories of the firms and their representatives. The SEC’s goal in designing the Form CRS template was “accessibility, brevity, and readability.” Dually registered RIAs are allowed four pages.

In addition, the form instructs firms to complete a “conversation starters” section to include at least three questions retail clients should ask of their advisor or point of contact, specifically to address some of the differences between a BD and an advisory firm. This section is included within the two-page format.

At a minimum, Form CRS must include the following sections:

- Firm registration information

- A description of all product and services offerings

- Full disclosure of fees and costs

- Disclosure of potential conflicts of interest

- The disciplinary history of the firm and its associates

- “Conversation starters”

Form CRS’s Strict Format Requirements are a Challenge

Given the brevity and page requirements, firms are finding the completion of Form CRS to be challenging. While the SEC has given firms an opportunity to create their own version of the form, it must be based on the prescribed question-and-answer format with specific headings. The wording used to describe services offered may be a combination of the specified language in the instructions and their own text, yet the section must include information on monitoring, limited investment offerings, account minimums, and other requirements.

The questions in the Conversation Starters section and specific references to Additional Information must be asked as prescribed and formatted to stand out from the other text in the form. However, they may be changed or omitted if they don’t apply to the firm’s business model.

To say that distilling all that information into two pages without omitting material facts is challenging is an understatement. It took the SEC more than 500 pages to outline the instructions for Form CRS. By some estimates, firms will spend, on average, nearly 24 hours and over $6,000 to complete the form.

Looking for a Form CRS Template?

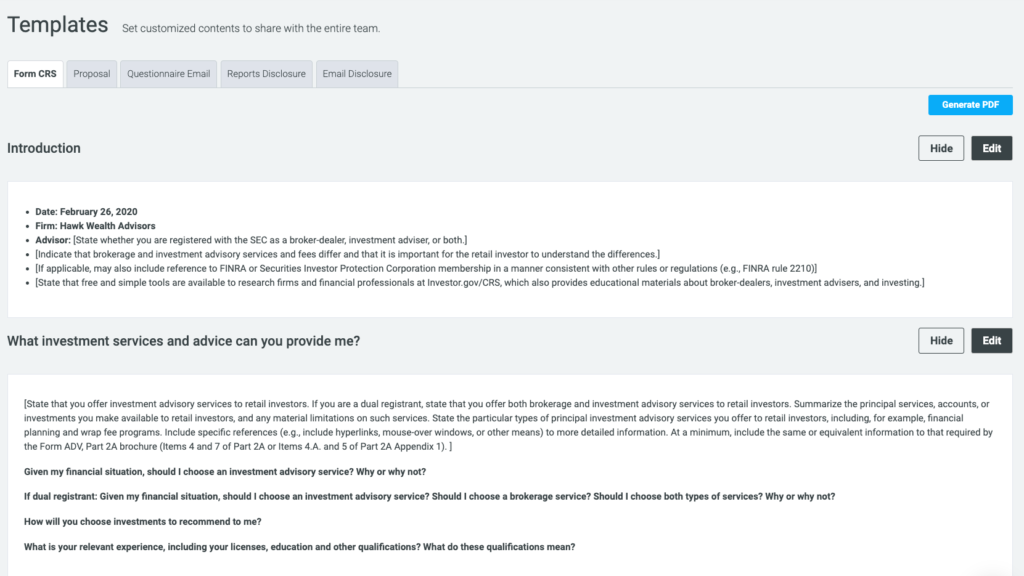

You can find a Form CRS template along with additional information at SEC.gov here Form CRS Instructions and here ADV Instructions. Users of Stratfi’s PRISM risk management platform can access a Form CRS template. As you can see from the screenshots below, the template is fully compliant with SEC requirements, enabling you to work efficiently through the its prescribed process. Each section includes the required heading questions along with approved questions that can be used in the conversation starter section.

Software to help you with Form CRS and RegBI

Source: Stratifi Technologies

StratiFi’s award-winning PRISM Rating™ technology already comes with a built in Form CRS template that is ready for advisors to use right out of the box. It uses the same guidelines provided by the SEC on SEC.gov. The Form CRS template is generated by our software to be fully customizable and can be branded for your firm.

Here are some additional resources for help with completing Form CRS and answering your questions:

- Full-Form CRS guidelines from the SECForm CRS summary and FAQ from the SEC

- Reg BI and Form CRS checklist from FINRA

Form CRS Deadlines and Timing for Client Delivery

The deadline for submitting Form CRS with the SEC was June 30, 2020. Going forward, RIAs and broker-dealers filing initial applications for registering with the SEC must file the form with their registration. Following their submission of the form, firms must meet specific delivery requirements in getting the form in their existing clients and prospective clients’ hands. Current clients must receive the form within 30 days of the filing date. The form may be delivered in an electronic format. The form must also be made available for public access through the SEC’s website, as well as the firm’s website.

On an ongoing basis, firms must adhere to the following delivery triggers:

- All advisors must provide a current copy of Form CRS to new clients at the time they enter into a contractual agreement.

- The form must be updated and submitted within 30 days of a material change that renders it inaccurate. Clients must be notified within 60 days of the new filing. The form must also be provided to retail investors upon request.

- BDs and dually registered firms are required to provide new and prospective clients with Form CRS at the earliest of

- Making a recommendation for an account type,

- Opening a new brokerage account for a retail investor

- Placing an order for a retail investor,

- Recommending an investment product, investment strategy involving securities, or an account change, including a retirement account rollover, or

- Recommending a new brokerage or investment service or investment that may not involve opening a new account and would not be held in an existing account.

Summary

Unquestionably, the implementation of Reg BI – along with the Form CRS requirements – has kept compliance departments hopping over the last year. Firms have had more than a year to bring their operations into compliance. They will now be subject to exams performed by FINRA and the SEC to ensure firms have made a “good faith” effort to “reasonably” comply with Reg BI up to this point, with the expectation they will be in full compliance at a later date. We can expect additional changes and fine-tuning of Reg BI and Form CRS when the results of the initial compliance audits are completed in the next several months.

The process of creating and distributing Form CRS has already proven to be challenging and costly, but all indications are it’s here to stay. Its purpose – to help inform retail investors of the differences between broker-dealers and RIAs and how they operate – is generally accepted among RIAs and has become a source of confusion among broker-dealers.

Then there’s the Department of Labor’s recent announcement of its “five “test regulation governing investment advice in retirement accounts. Though it’s not in conflict with Reg BI, it will add another layer of compliance. The new DOL regulation replaces the “fiduciary rule” that was vacated by a federal appeals court more than two years ago.

All in all, it’s shaping up to be a game-changing year for the investment industry.