Table Of Contents

To support growth, RIAs have spent years building comprehensive technology stacks by combining CRM systems, portfolio management tools, risk assessment software, compliance solutions, and reporting platforms. While each tool solves a specific function, most firms face a new challenge: critical data, workflows, and oversight being disconnected.

As regulatory scrutiny increases and client portfolios become more complex, RIAs are expected to demonstrate continuous alignment between advice, risk, and supervision, rather than reconstructing it after decisions are made.

The concept of a unified wealth platform emerged in response to this fragmentation. Rather than adding another tool, it represents an operating model shift: connecting data and workflows across advisory, risk, and compliance functions so oversight happens alongside advice.

For modern RIAs, unification is shifting from a focus on efficiency to one of maintaining transparency, scalability, and trust as firms evolve.

What Is a Unified Wealth Platform?

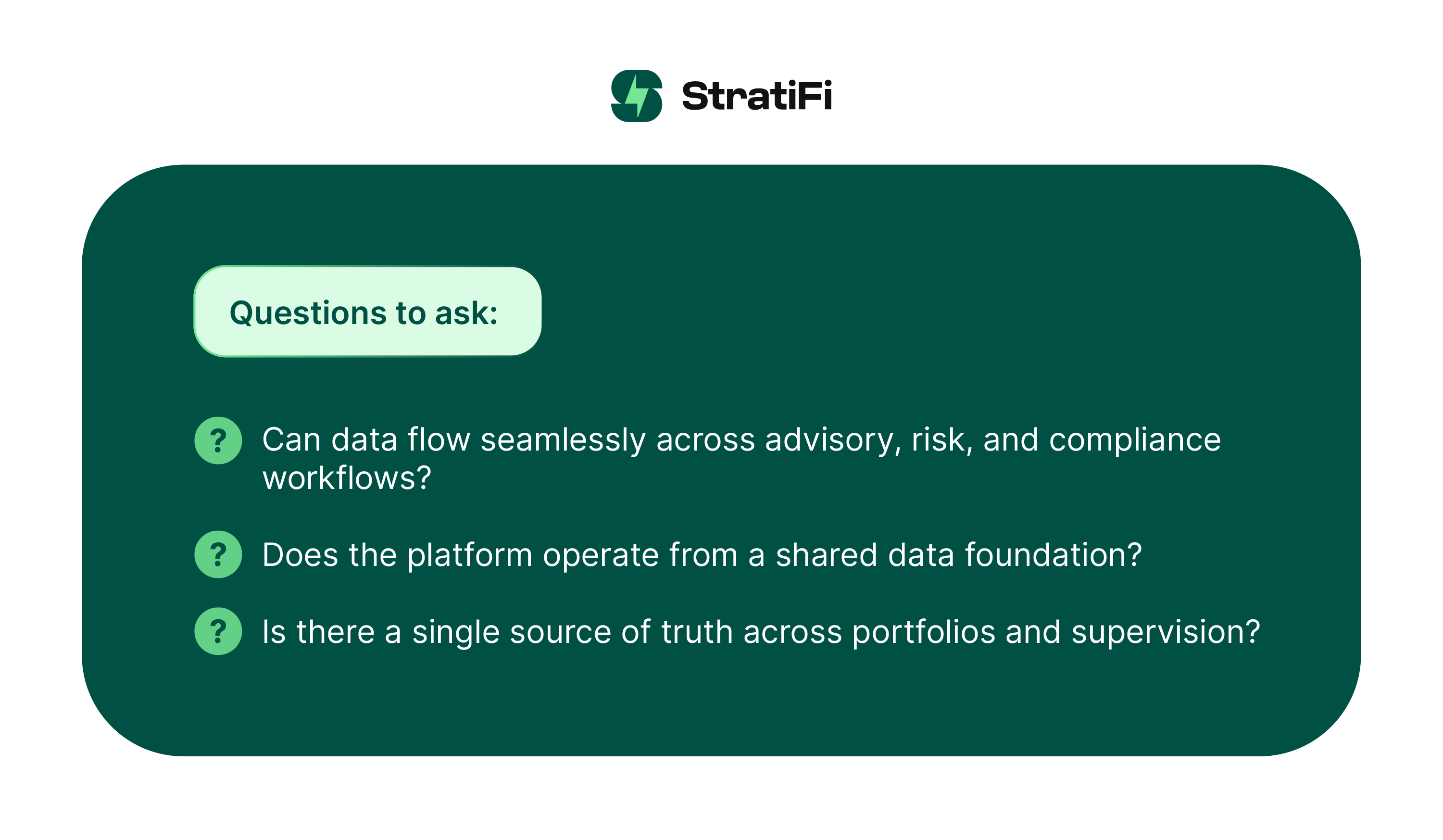

A unified wealth platform is a technology operating layer that connects data, workflows, and oversight across advisory, risk, and compliance functions within a single environment. It doesn’t treat portfolio management, advisor workflows, and supervision as separate systems; rather, it ensures that each activity shares the same underlying data and context.

In traditional environments, advisors create recommendations in one system, risk is analyzed in another, and compliance documentation is maintained elsewhere.

A unified wealth platform removes these handoffs by keeping portfolios, client objectives, risk intelligence, and supervisory monitoring continuously connected. As advice evolves, oversight evolves alongside.

This connected model allows advisory teams to work from a shared foundation:

- Advisors can develop proposals and client reviews using integrated portfolio and behavioral risk insights

- Compliance teams monitor the same portfolios through automated surveillance and suitability documentation

- Leadership gains firm-wide visibility without relying on manual reconciliation across tools.

The value a unified wealth platform brings comes from connected workflows, ensuring that decisions, risk evaluation, and documentation remain aligned from initial client engagement through ongoing monitoring.

Modern unified wealth platforms achieve this by combining several capabilities within a common data model:

- Advisor workflows that support proposals, investment policy development, and ongoing client engagement

- Continuous compliance monitoring that detects drift, concentration risk, and suitability concerns automatically

- Operational automation that reduces manual recordkeeping and reconciliation work

- Shared intelligence that enables investment insights and oversight to scale across the firm

By unifying these functions, the platform transforms compliance and risk management from downstream review processes into embedded parts of everyday advisory activity.

The result is an environment where advice, risk, and supervision move together, allowing RIAs to operate more efficiently while strengthening transparency and defensibility.

What a Unified Wealth Platform Is Not

A unified wealth platform is often confused with existing technology categories. It differs in important ways:

- Not an “all-in-one” tool. It does not bundle features while leaving workflows disconnected; unified platforms connect actions across advisory, risk, and oversight.

- Not a CRM replacement. CRMs manage relationships and pipelines, while unified platforms align investment decisions with supervision and risk context.

- Not just compliance software. Documentation alone records activity; unlike finance compliance software, unified platforms embed monitoring and evidence creation into daily workflows, allowing for seamless integration.

- Not a reporting dashboard. Dashboards summarize outcomes after the fact; unified platforms enable continuous visibility as decisions happen.

The core difference: With a unified wealth platform in place, workflows remain connected, allowing advice, risk, and supervision to evolve together.

The Problem with the Traditional Tech Stack

Most RIAs operate using a collection of specialized point solutions, each designed to solve a specific function like CRM, portfolio accounting, risk analysis, compliance monitoring, document storage, and reporting. While effective individually, these systems were not designed to work as a connected operating environment.

How RIAs Operate Today

Advisory firms typically rely on multiple independent tools:

- CRM systems for client relationships

- Portfolio and performance platforms

- Risk and proposal tools

- Compliance and surveillance software/processes

- Reporting and document management systems

In practice, advisors and compliance teams become the integration layer, manually connecting information across systems. Simply put, humans connect the dots.

Where Point Solutions Create Risk

- Duplicate data and conflicting records across platforms

- Manual reconciliation between portfolios, risk analysis, and compliance reviews

- Documentation created after decisions, increasing exam exposure

- Limited real-time visibility for leadership and supervisors

- Operational dependence on spreadsheets and human memory

As firms grow, the challenge shifts from having enough tools to ensuring those tools produce a consistent, defensible view of advice and oversight. Point solutions optimize individual tasks, but fragmentation introduces operational and regulatory risk.

Why RIAs Need to Move beyond the Traditional Tech Stack

The limitations of fragmented systems are becoming more visible as advisory firms scale and regulatory expectations evolve. What once worked for smaller teams managing simpler portfolios now creates operational friction and oversight gaps.

Several industry shifts are accelerating the move toward unified platforms:

- Increased regulatory scrutiny: SEC exams increasingly evaluate ongoing supervision and documented alignment between advice and client outcomes.

- Reg BI and suitability expectations: Oversight must extend beyond initial recommendations to continuous monitoring.

- More complex client households and products: Portfolios change frequently, requiring risk and compliance context to update in real time.

- Advisor growth without proportional compliance hiring: Firms must scale oversight without expanding headcount at the same pace.

- Higher client expectations for transparency and consistency: Institutional-grade practices are becoming standard across advisory firms.

As these pressures converge, the real challenge is ensuring that advice, risk, and oversight remain continuously connected across the organization.

Unified wealth platforms emerge as a response to this operational reality.

Enter the Unified Wealth Platform: The Core Components

A unified wealth platform brings together the systems RIAs traditionally manage separately into a connected operational foundation. Instead of synchronizing tools after work is completed, the platform ensures that data, workflows, and oversight remain aligned as activities occur.

Key components typically include:

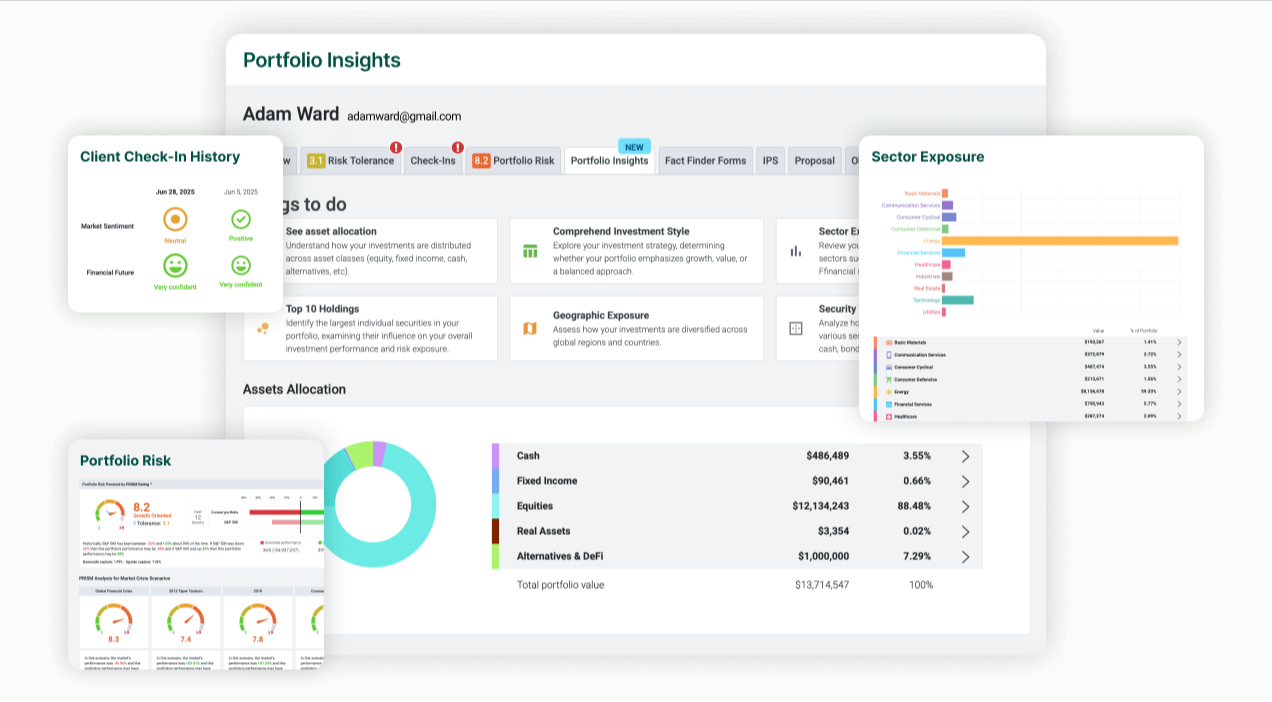

- Unified Data Foundation

Client, portfolio, risk, and documentation data exist within a shared environment. Advisors, compliance teams, and leadership operate from the same information, eliminating reconciliation across multiple systems and reducing inconsistencies.

- Connected Workflows across Teams

Advisor activities, from proposals and investment policy creation to client reviews, are directly linked to portfolio data and risk context, allowing decisions to carry forward into monitoring and supervision automatically.

- Embedded Risk and Suitability Context

Risk evaluation is integrated into daily workflows rather than performed as a separate analysis. Portfolio changes, client objectives, and behavioral risk insights remain continuously connected.

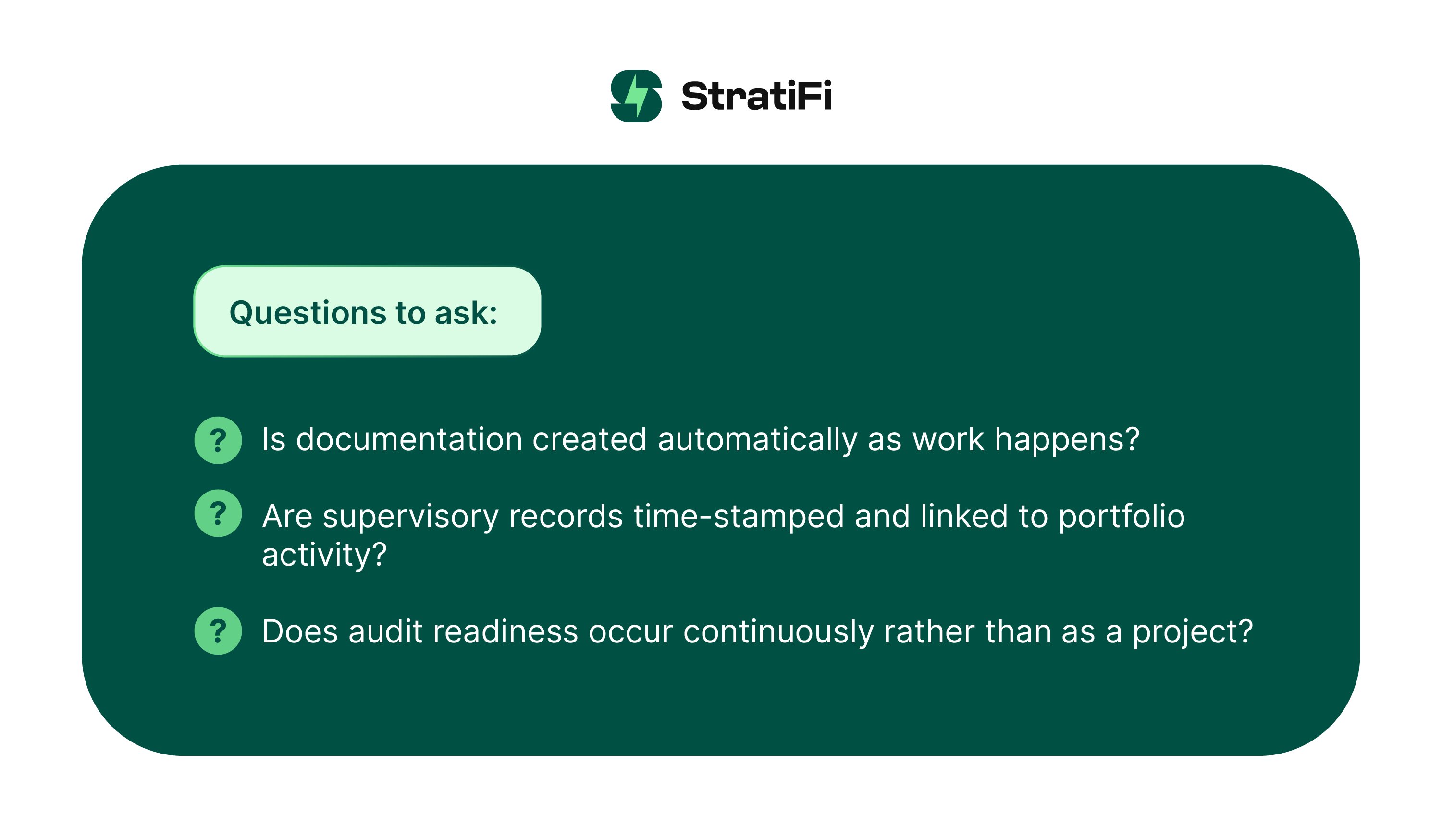

- Continuous Documentation

Supervisory records and suitability documentation are created alongside advisory activity, making audit readiness an ongoing outcome instead of a manual project.

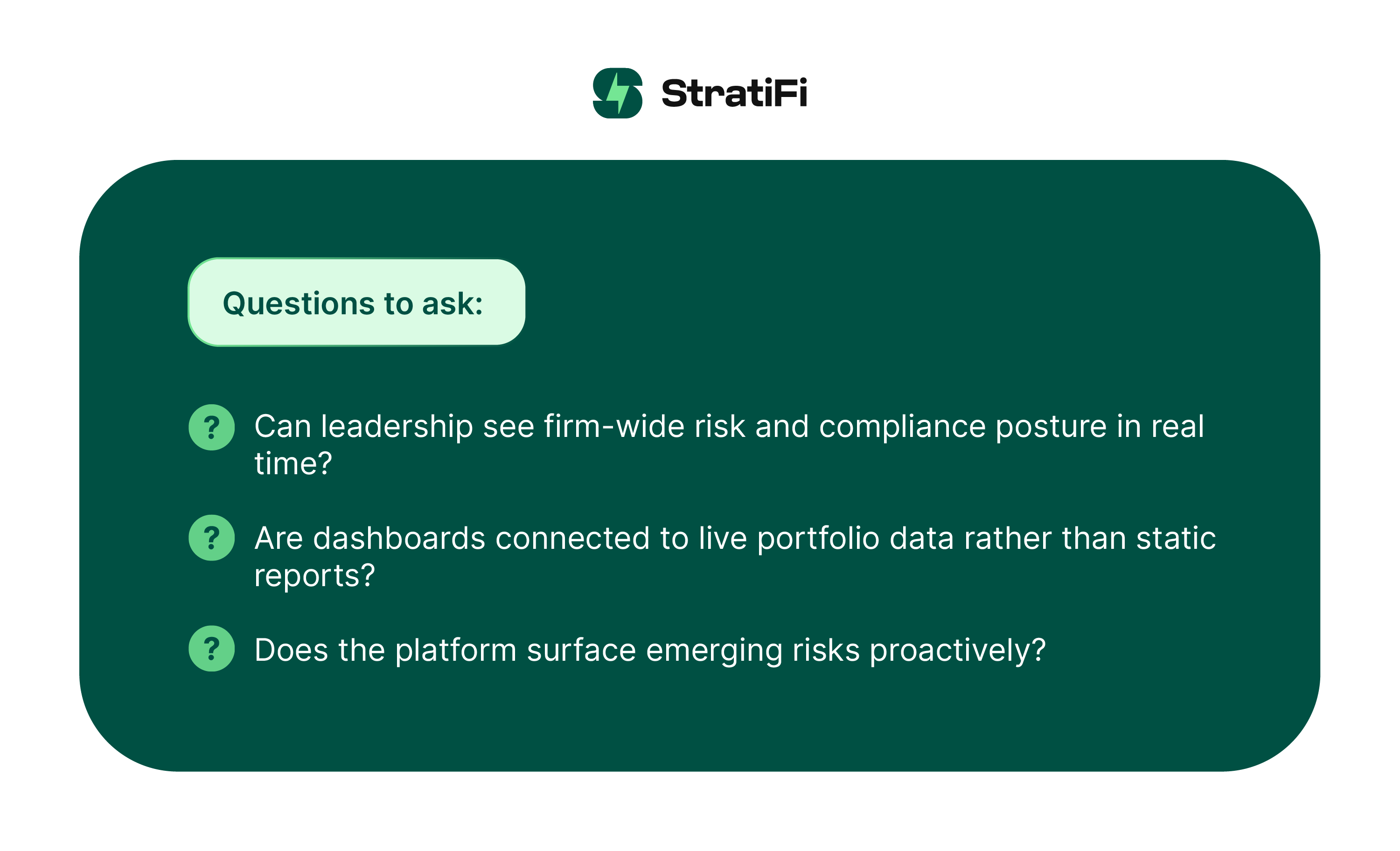

- Firm-Wide Visibility

Leadership and compliance teams gain real-time insight across advisors and accounts, enabling proactive oversight rather than retrospective review.

Together, these components transform technology from a collection of tools into a unified operating layer where advice, risk management, and supervision evolve together.

How Modern Unified Wealth Platforms Transform Risk Management

Traditional risk management in advisory firms often operates as a periodic exercise:

- Portfolios are reviewed at intervals

- Risks are analyzed separately, and

- Findings are documented after changes occur

Unified wealth management platforms impact risk management in the following ways:

- Risk evaluation is built into daily workflows

Modern wealth management platforms embed risk assessment directly into everyday advisory workflows rather than treating it as a separate or periodic activity.

- Continuous risk assessment

Portfolio, client, and behavioral data exist within a shared environment; hence, risk can be evaluated continuously instead of retrospectively. When allocations change or market conditions shift, exposure is assessed in context and linked to client objectives and suitability considerations in real time.

- Holistic risk monitoring

Risk monitoring extends beyond the common performance metrics. Advisors can evaluate portfolio drift, concentration exposure, liquidity factors, and suitability signals together, offering a clearer understanding of why the risk profile changes, not just how the portfolio performs.

- Proactive oversight for RIAs

The connected approach allows RIAs to move from reactive portfolio reviews to proactive oversight, allowing advisors to address potential risks before they escalate.

- Improved communication and organizational visibility

Advisors gain clearer ways to communicate risk during client interactions, while compliance and leadership teams maintain consistent visibility across accounts and portfolios.

- Risk management becomes an ongoing strategic process

Risk management becomes a continuous, explainable process rather than a periodic compliance exercise, helping reduce operational uncertainty and strengthen decision-making confidence across the firm.

How Unified Wealth Platforms Support Compliance and Supervision

In many advisory firms, compliance operates downstream from advisory activity:

- Reviews occur after trades

- Documentation is assembled separately, and

- Supervision relies on periodic sampling

Unified wealth platforms for supervision and compliance change this scenario by embedding supervision directly into daily workflows.

Because advisory activity, portfolio data, and risk context share the same foundation, compliance teams monitor the same information advisors use to make decisions. This allows supervision to become continuous rather than episodic.

Portfolio drift, concentration exposure, trading patterns, and suitability signals can be identified automatically as they emerge, instead of waiting for scheduled reviews.

Modern unified wealth platforms for RIA operations also align documentation with decision-making. Client reviews, suitability records, and supervisory evidence are created alongside advisory actions, helping firms maintain audit readiness without manual reconstruction during exams.

The result is not automation replacing compliance professionals. Still, technology is giving them greater leverage, enabling consistent oversight across advisors and accounts while reducing dependence on spreadsheets, fragmented systems, and retrospective reviews.

5 Problems a Unified Wealth Platform Solves (And What RIAs Should Look for)

As firms evaluate a unified wealth platform, the right question is not “What features does it have?” but “What operational risks does it eliminate?”

Below are the most common challenges fragmented tech stacks create. When these problems are solved collectively, RIAs move beyond disconnected tech stacks toward an operating model where advice, risk, and supervision remain aligned in real time.

1. Fragmented Oversight across Systems

Advisory, risk, and compliance tools operate independently, forcing teams to connect information manually.

RIAs should look for a true unified wealth management platform that connects these workflows instead of relying on humans to reconcile them.

2. Reactive Documentation and Audit Stress

Documentation is often created after decisions are made, increasing regulatory exposure during exams.

RIAs must opt for unified wealth platforms for compliance and embed documentation into daily operations, reducing reconstruction risk.

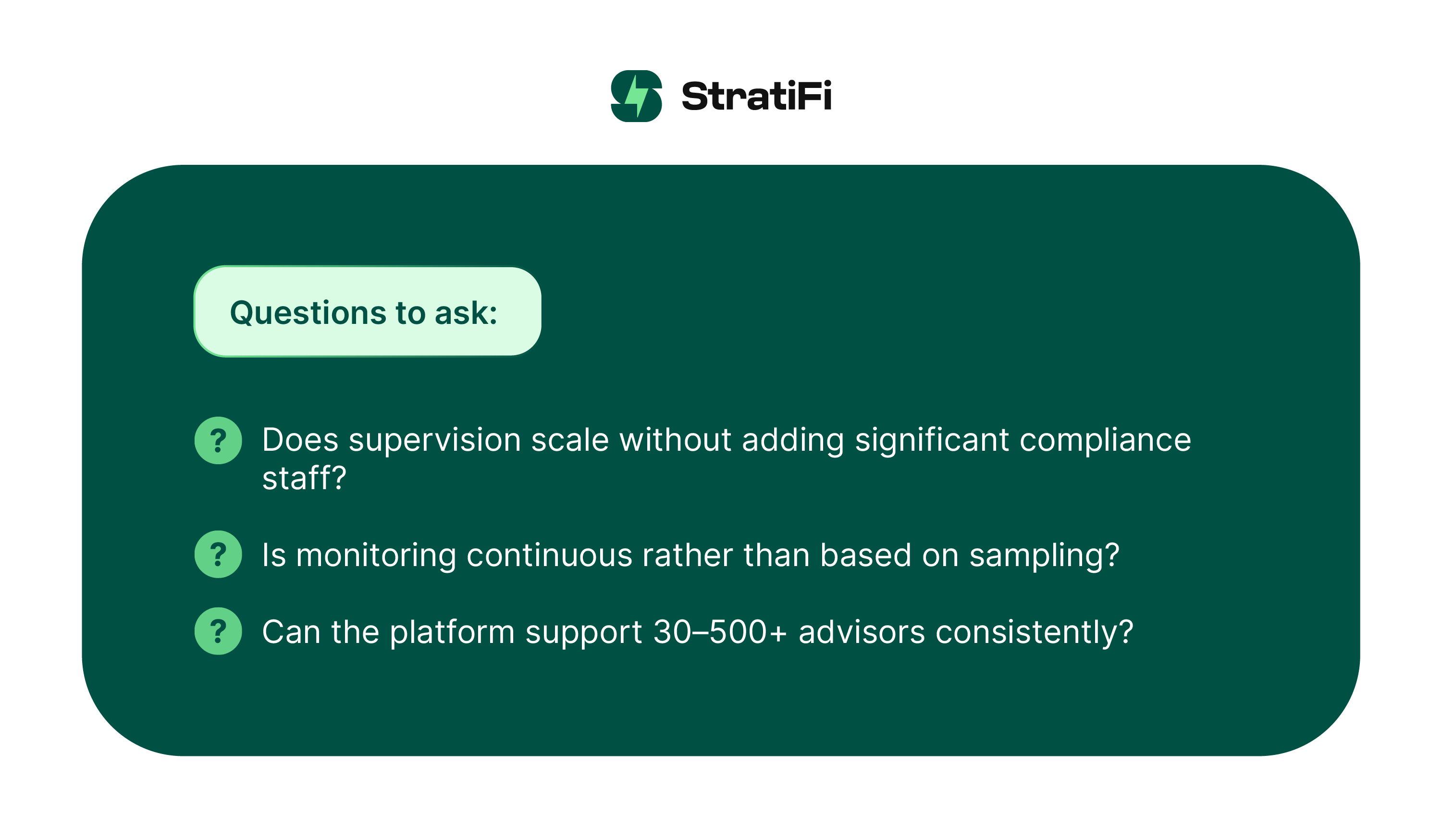

3. Supervision That Doesn’t Scale

As the advisor count grows, the compliance headcount must grow proportionally, unless oversight is automated.

Modern unified wealth platforms for registered investment advisors help firms scale oversight efficiently.

4. Limited Firm-Wide Visibility

Leadership lacks real-time insight into portfolio risk, suitability exposure, or supervisory gaps. Unified advisor platforms provide visibility not just into activity, but into risk alignment across the organization.

5. Manual Reconciliation and Operational Drag

Teams spend hours reconciling spreadsheets, updating systems, and verifying consistency across tools. A unified wealth technology platform should reduce operational risk by eliminating repetitive manual coordination.

The Shift from Scattered Tech Stack to Unified Operating Model

For years, advisory firms approached growth by adding specialized tools to their tech stacks. But as portfolios become more complex and regulatory expectations intensify, the challenge is no longer access to technology; it is alignment.

A unified wealth platform represents a shift from fragmented systems toward a connected operating model. When advisory workflows, risk intelligence, and supervision operate from the same foundation, firms reduce operational friction while strengthening transparency and defensibility.

Continuous oversight replaces periodic review. Documentation becomes embedded rather than reconstructed. Leadership gains real-time visibility across advisors and accounts.

For modern RIAs, unification is not about replacing every tool but about ensuring that advice, risk, and compliance move together as the firm scales. The firms that adopt unified wealth platforms for RIAs are not simply optimizing efficiency; they are building infrastructure designed for resilience, audit readiness, and long-term trust.

Explore unified wealth management in practice.

See how connected advisory workflows and continuous compliance monitoring work together within a unified operating environment.

Book a demo now to learn how StratiFi supports unified wealth management for modern RIAs.

FAQs

What Is a Unified Wealth Platform?

A unified wealth platform is a connected operating system that integrates advisory workflows, portfolio data, risk management, and compliance oversight into a shared environment. Unlike fragmented tech stacks, it keeps advice, risk, and supervision aligned in real time.

How Is a Unified Wealth Platform Different from a Tech Stack?

A traditional tech stack consists of separate tools that require manual coordination. A unified wealth platform connects data and workflows across systems, allowing advisory, risk, and compliance functions to operate from a single, integrated foundation.

How Does a Unified Wealth Platform Support Compliance?

Unified wealth platforms embed supervision and documentation directly into advisory workflows. Monitoring, suitability tracking, and audit trails are created continuously, reducing reliance on retrospective reviews and improving exam readiness for RIAs.

Can a Unified Wealth Platform Reduce Operational Risk?

Yes. By eliminating manual reconciliation between systems and connecting workflows across teams, unified wealth platforms reduce data inconsistencies, documentation gaps, and supervisory blind spots that can increase regulatory and operational risk.

What Should RIAs Look for in a Unified Wealth Platform?

RIAs should look for shared data foundations, continuous risk monitoring, embedded documentation, scalable supervision, and real-time firm-wide visibility. The platform should reduce manual work while strengthening alignment between advisory decisions and oversight.